With so much media attention spotlighting retirement planning these days, you would think the United States is a nation of hardcore investors, well-versed in the intricacies of all sorts of financial products. But the truth is most Americans know relatively little about one of the most effective tools for securing their financial futures: the Individual Retirement Account (IRA).

With so much media attention spotlighting retirement planning these days, you would think the United States is a nation of hardcore investors, well-versed in the intricacies of all sorts of financial products. But the truth is most Americans know relatively little about one of the most effective tools for securing their financial futures: the Individual Retirement Account (IRA).

Indeed, only 33.4% of Americans’ retirement assets reside in IRA accounts. That may be due in part to a lack of understanding about what an IRA is and how you can use it to help you towards achieving your financial goals.

Investment Flexibility

Opening an IRA account enables investors to take advantage of many different investment products, including mutual funds, stocks, bonds, exchange-traded funds and REITs. Virtually any security that can be owned outside an IRA can be owned inside an IRA.

This is important to understand because it gives investors the flexibility and latitude to help towards reaching their financial goals, whether they are short-term or long-term. Knowing what an IRA is can be a good start but knowing how to use it effectively should be the goal of any investor.

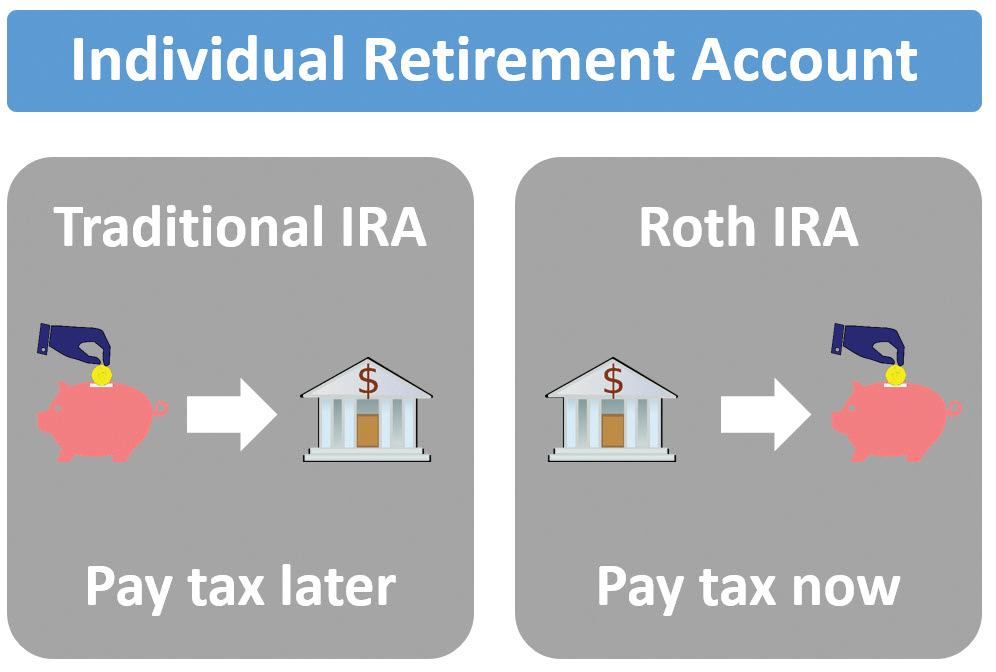

You should take some time to understand the difference between a traditional and a Roth IRA. In short, contributions to Roth IRAs are made with after-tax dollars and qualified withdrawals are tax free. By contrast, contributions to traditional IRAs may be tax-deductible, but withdrawals are taxed as ordinary income. Your adjusted gross income and participation in a retirement plan will determine if a traditional IRA is deductible.

In addition, your adjusted gross income will determine if you can contribute to a Roth IRA. You can always contribute to a non-deductible traditional IRA if you do not qualify for a Roth or a deductible traditional IRA. IRA withdrawals from a traditional IRA, if taken prior to age 59 ½, may be subject to an additional 10% federal tax penalty and possibly state income taxes. Qualified distributions of earnings from a Roth IRA are tax-exempt after five years from the contribution date and after age 59 ½. Earnings taken prior to age 59 ½, may be subject to a 10% federal tax penalty and possibly state income taxes.

Regardless of whether it is Roth or traditional, a major benefit of an IRA is that it may own a variety of investments. In other words, you can find the investment vehicles that match your goals and risk tolerance, from long-term and aggressive to short-term and cautious. Certainly, a mixture of mutual funds, stocks and bonds within an IRA can help achieve the sort of diversity that most investors seek.

Inherited IRAs

Inherited IRAs

Making the most of an IRA can also mean managing an inherited one appropriately. Indeed, mishandling an inherited IRA is a common—and expensive—mistake. If you are the beneficiary of an IRA, it is important to get competent advice before receiving the money.

Proper titling is crucial. If the IRA is titled correctly, you can receive distributions over your lifetime as a spouse or 10 years as a non-spouse beneficiary. For example, a custodian may require that an account be titled as follows if it involves a father, John Jones, who dies and leaves an IRA to his son, Sam: John Jones, deceased (date of death), IRA for the benefit of Sam Jones. Titling the account properly enables Sam to take distributions over his lifetime, which can potentially add a lot of value to an IRA by allowing additional growth potential over many years.